How do you calculate ownership percentage?

Let’s say you own one million shares of a startup company. (Good for you. Yay, you!) So what is your percentage of ownership in the company? It sounds like a straightforward question, but the answer depends on how you do the math.

This isn’t a case of figures lying or liars figuring, as the old saying goes. Different methods for calculating your percentage of ownership will be used depending on who you are and the reason the question is being asked.

Basic Ownership Percentage Calculation

The basic equation is so simple a middle schooler can solve it:

The tricky part is deciding the denominator in that equation. The main variable being how options and the option pool get counted in the total shares. Two common ways of computing this:

Understanding Issued and Outstanding Shares

- Issued and Outstanding refers to the number of shares actually held by the company’s stockholders. This includes common stock and preferred stock. Preferred stock should be counted as if it were converted to common stock (via the conversion ratio for each stock class). Stock options are not included.

What Does Fully Diluted Ownership Mean?

- Fully Diluted means shares currently held by stockholders, plus all options and shares reserved for future grants. Included are incentive stock options granted to employees, warrants issued to other entities, and any other security that converts to common stock. The remainder of the stock option pool is also added. (Take note that sometimes the term “fully diluted” gets bandied about without always being precise to this definition.)

By the way, the total authorized shares for the company doesn’t matter when you are considering a percentage of ownership and would never be used in this calculation.

Since fully diluted is the superset, a percentage of ownership based on fully diluted shares will always be lower than one calculated based on issued and outstanding shares. Let’s look at the difference between these two methods with some sample numbers. Assume the company has:

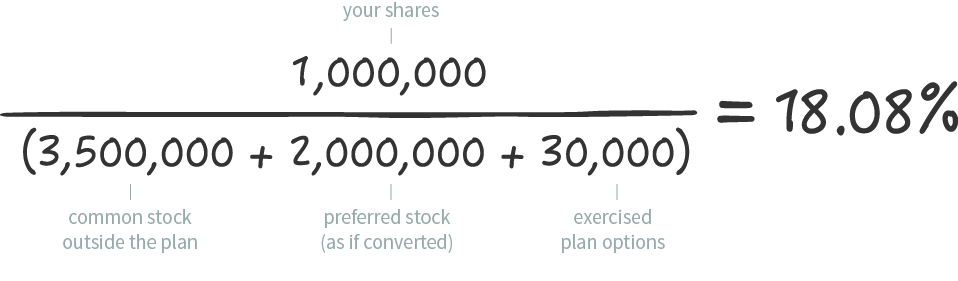

- Common stock issued outside the plan: 3,500,000

- Preferred stock issued (as converted to common): 2,000,000

- Options granted under the plan and exercised: 30,000

- Options granted under the plan but not exercised (vested and unvested): 70,000

- Options remaining in the plan: 400,000

- Warrants: 600,000

Example Ownership Percentage Calculation for 1 Million Shares

The ownership percentage for your one million shares based on issued and outstanding:

And, based on fully diluted:

Which numbers should you use to calculate company ownership?

Do you own 18% or 15%? Here’s where it’s helpful to understand the context and the motivations. Do you want to know what is accurate at this exact moment or is it a speculative question? Are you looking for the best case or worst-case scenario?

Other Factors That Impact Ownership Calculations

If there is a transaction happening today—perhaps a stockholder vote is occurring—only the shares that are actually owned right now are going to matter. So issued and outstanding is the useful calculation. Only current stockholders are eligible to participate in the vote.

On the other hand, investors are typically forward-looking and think of things in fully diluted terms. By assuming that the company will continue to grow, the entire stock option pool is granted, and every single share is exercised, they can see the most conservative estimate of what their ownership will be. This detailed perspective is important when thinking about future control of the company and modeling for possible outcomes.

Other cases can be more complex. If there is an upcoming liquidity event, it would also make sense to factor in any in-flight transactions that will grant shares and any vested options that may be exercised beyond what is currently held.

With each new stock issuance or fundraising the numbers are adjusted, dilution occurs, and percentages must be recalculated. One thing you can likely count on is that your ownership percentage is going to change—regardless of how you do the math!

Want to manage ownership without the headache? Let's talk about how Fidelity can help.

Sample scenarios are for illustrative purposes only. A link to third-party material is included for your convenience. The content owner is not affiliated with Fidelity and is solely responsible for the information and services it provides. Fidelity disclaims any liability arising from your use of such information or services. Review the new site's terms, conditions, and privacy policy, as they will be different from those of Fidelity's sites.

1093706.2.0