One of the most important documents in a traditional equity financing is the Stock Purchase Agreement (SPA). Entrepreneurs will often agonize over pre-money valuation liquidation preference, etc. (and rightfully so). However, the Representations and Warranties, and accompanying Disclosure Schedule, are also very important to think through and get right. In these sections of the SPA, the company represents what it knows to be true about the company, and then identifies areas where those representations need qualifications and exclusions.

Investors have limited options for learning about the business and its related risks. Typically, they learn about the business through the CEO, usually in the pitch deck and a few other ways. And even then, the only information that the investors receive generally relates to the company’s ideas, market, technology, prospective financials, and team members.

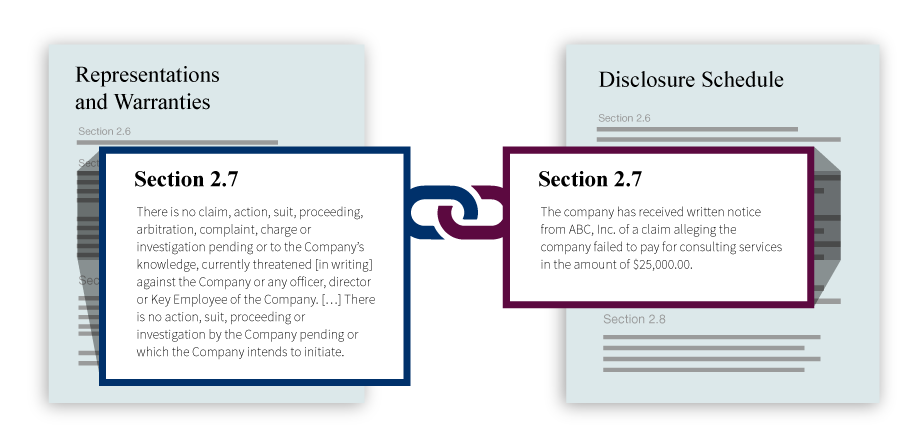

Representations and Warranties

The company’s portion of the Representations and Warranties is largely boilerplate, though it may be negotiated based on the applicable technology and associated degree of risk. In other words, most SPAs contain a very similar set of representations which are (generally) accepted by most technology investors. For example, in areas like litigation, the company states there are no lawsuits against the company. In areas like intellectual property, the company states that it owns all of its IP necessary to run the business. But what if there are exceptions to the representations as written? For this information, investors turn to the Disclosure Schedule.

Disclosure Schedule

The Disclosure Schedule is the part of the Stock Purchase Agreement where you list the exceptions to the statements made in the Representations and Warranties. For example, your representation around litigation stated that you have no pending lawsuits against you—but what if you do? Let's say an employee is suing you for wrongful termination. This fact (this exception to the representation) would be listed in the Disclosure Schedule. A company usually states that it has full rights to all of the IP it uses in the Representations and Warranties section, but then may state in the Disclosure Schedule that, in fact, it relies on the use of certain patents licensed to it by a third party.

Because of the nature of the SPA, investors pay very close attention to the Disclosure Schedule. They look there for details about the challenges the business is facing—it’s where the company airs its dirty laundry.

How Much Do I Disclose?

In many ways, putting together a Disclosure Schedule seems fairly straight forward—you made a representation in Representations and Warranties, and now you’re stating an exception. But those exceptions expose to investors the potential risks the company is facing. The Disclosure Schedule is your way of protecting yourself down the road should an investor claim that you misrepresented an aspect of your company (and potentially demands their money back). The balancing act is to make sure you are making the appropriate disclosures, without spooking your investors. In this regard, writing the Disclosure Schedule is an art, one of those areas best navigated with your counsel to make sure you maximize protecting your company while demonstrating that it is an attractive investment.

Learn more about the data room capabilities in Fidelity.

1096553.1.0